What if your next roof replacement wasn’t a drain on your 2026 operating capital, but actually served as your most strategic tax move of the year? Many business owners in the Portland and Vancouver metro areas face the same dilemma of balancing high upfront costs for flat-roof systems against the need to keep credit lines open for core operations. You already know that delaying a project during a wet Northwest winter only leads to more expensive structural damage, yet the timing for a major capital expenditure rarely feels perfect.

This guide will show you how to utilize the best commercial roof replacement financing options to protect your facility without compromising your cash flow. We’ll explore how to leverage the current $2,560,000 Section 179 deduction limit, tap into local incentives like the $2.00 per square foot Energy Trust of Oregon rebate, and secure fixed monthly payments that align with your revenue cycles. You’ll learn how to transform a necessary maintenance task into a warrantied asset that provides immediate tax benefits and long-term peace of mind for your Northwest business.

Key Takeaways

- Learn how to preserve your business credit lines by treating a new roof as a strategic financial asset rather than an immediate cash drain.

- Discover the 2026 tax advantages of Section 179, which may allow you to deduct the full cost of your roof replacement in the first year.

- Compare the most competitive commercial roof replacement financing options available to Portland and Vancouver metro area businesses.

- Follow a simple five-step roadmap to organize your financial records and roof condition reports for a faster, easier approval process.

- See why partnering with a family-owned Northwest expert provides the long-term protection and stability your facility needs to withstand local rain and wind.

Navigating Commercial Roof Replacement Financing in the Pacific Northwest

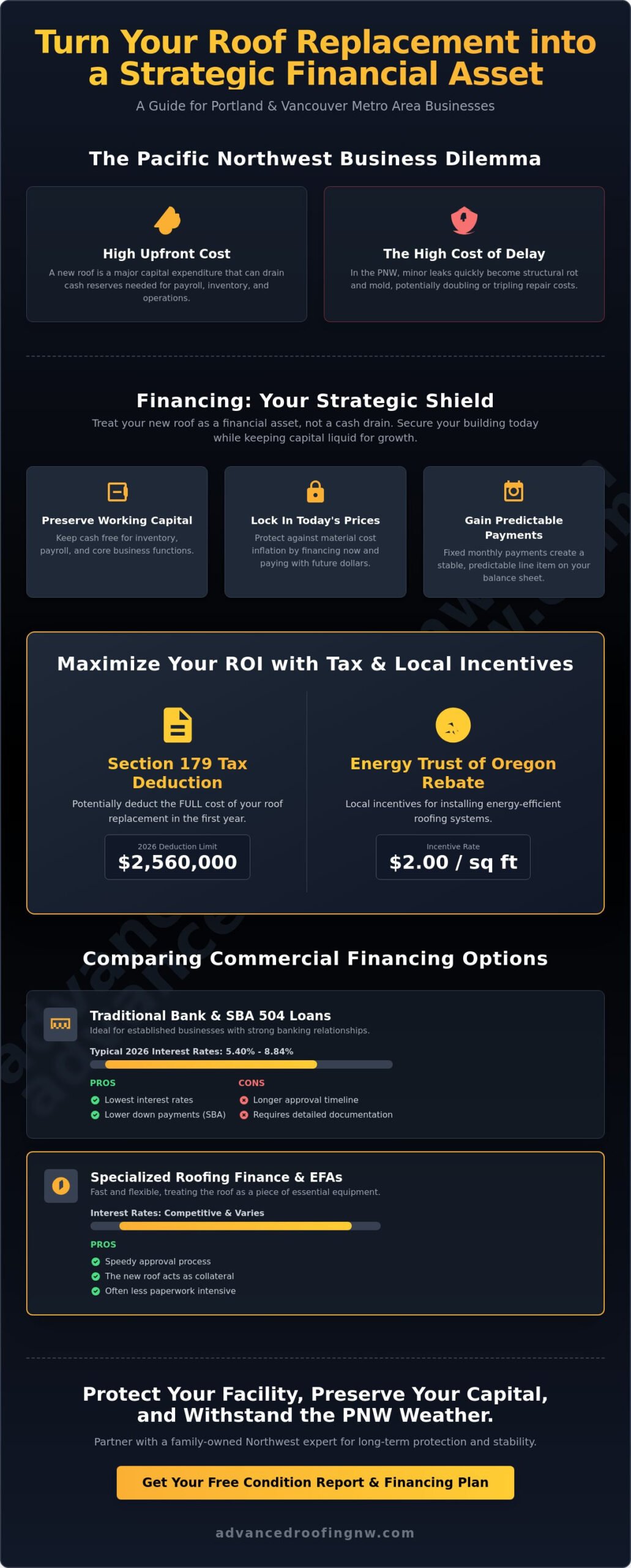

Think of commercial roof financing as a strategic shield for your business assets. It is a specialized credit tool that allows you to address critical facility needs without depleting the cash reserves you need for daily operations. In the Portland and Vancouver metro areas, where rain is a constant companion, waiting for a “better time” to fund a project often leads to compounding expenses. By exploring commercial roof replacement financing options, you can secure your building’s integrity today while keeping your capital liquid for growth and unexpected opportunities.

Why Cash is Not Always King in Commercial Roofing

Writing a large check for a roof replacement might seem like the simplest route, but it often isn’t the most efficient use of your resources. Preserving working capital is vital for managing inventory, meeting payroll, and staying agile in a competitive market. When you use external business loan options to fund your project, you maintain your liquid assets for core business functions. This approach also protects you from the rising costs of roofing materials. Inflation can drive up the price of TPO or PVC systems significantly over a few years; financing allows you to lock in today’s prices and pay them back with tomorrow’s dollars. Fixed-rate payments provide a level of predictability that is invaluable in a fluctuating economy, ensuring your facility costs remain a stable line item on your balance sheet.

The PNW Risk Factor: When Delaying Becomes More Expensive

In our corner of the Northwest, a minor leak rarely stays minor for long. Persistent rain and high humidity create a perfect storm for structural rot, especially in flat roof systems where ponding water is common. Water is patient. It finds every weakness. Delaying a replacement doesn’t just mean a higher roofing bill later; it often leads to the added expense of mold remediation and structural timber repair. These secondary issues can double or triple the total project cost. Beyond the physical structure, a failing roof threatens your tenant relationships and business reputation. Proactive facility management through commercial roof replacement financing options ensures your tenants stay dry and your operations remain uninterrupted. A master craftsman from a certified local team can provide a detailed condition report, which serves as a vital document when presenting your case to a lender. This partnership ensures the technical reality of your roof aligns perfectly with your financial strategy.

Comparing Your Commercial Roofing Loan and Credit Options

Selecting the right path from the various commercial roof replacement financing options depends on your business’s immediate cash needs and long-term tax strategy. Most Northwest property owners choose between four primary vehicles: traditional bank loans, SBA-backed programs, specialized equipment financing, or property-assessed clean energy programs. While traditional lenders offer stability, specialized roofing finance companies often provide more flexibility regarding how the roof itself serves as collateral. In many cases, the new roofing system acts as the security for the debt; however, small business owners should be prepared for lenders to request a personal guarantee to secure the most favorable interest rates.

Traditional Commercial Bank Loans and SBA 504

If you have a long-standing relationship with a local Portland or Vancouver bank, a conventional commercial loan might offer the lowest rates. As of May 2026, conventional commercial loan rates typically range from 5.40% to 8.84%. For larger projects, SBA-guaranteed loans provide an excellent alternative with lower down payments. The SBA 504 program is specifically designed for major fixed-asset improvements, offering rates between 5.88% and 6.02% for 2026. While these options provide great terms, the approval timeline can span several weeks, so they require early planning before the rainy season begins. A professional commercial roof inspection can provide the detailed condition report these lenders require during the underwriting process.

Specialized Roofing Finance and EFAs

Equipment Financing Agreements (EFAs) have become a preferred choice for many PNW businesses because they treat a roof replacement like a piece of essential machinery. The primary advantage here is speed. Approvals often arrive within 24 to 48 hours, which is critical if you’re dealing with active leaks that threaten your inventory. Many roofing contractors now partner with lenders to offer these integrated commercial roof replacement financing options, with some rates starting as low as 7.99% APR. You can often choose between fixed-rate terms that protect you from market volatility or floating options if you plan to pay the balance off early.

C-PACE Financing for Energy-Efficient Roofs

Commercial Property Assessed Clean Energy (C-PACE) is a unique tool available in Oregon and Washington that funds 100% of the project cost for energy-efficient upgrades. Unlike traditional loans, C-PACE is tied to the property itself rather than your business credit score. You repay the investment through a long-term assessment on your property tax bill, often extending up to 20 years. This is an ideal solution for businesses installing high-reflectivity TPO or enhanced insulation systems, as the energy savings often offset the annual tax payment. It’s a neighborly way to upgrade your facility’s protection while improving the local community’s energy footprint.

Maximizing ROI: Section 179 Tax Deductions and Local Incentives

Protecting your facility’s integrity is a physical necessity, but the financial structure of the project is what determines your true return on investment. For many Northwest business owners, the most powerful tool in the shed isn’t a roofing torch; it’s the federal tax code. For the 2026 tax year, the Section 179 deduction allows businesses to expense up to $2,560,000 of qualifying equipment and property improvements, including commercial roof replacements. This means you can often deduct the entire cost of your new roofing system in the same year it’s placed in service, rather than depreciating it slowly over decades. When you combine this immediate tax shield with various commercial roof replacement financing options, you create a unique synergy. Your tax savings in year one can often exceed the total sum of your first year’s financing payments, making the upgrade feel practically interest-free during the initial phase of the loan.

The Section 179 Advantage for Commercial Property

The 2026 deduction limit is generous, but it’s designed for active businesses. The phase-out threshold begins only after you’ve purchased more than $4,090,000 in qualifying equipment, ensuring that small to mid-sized Portland and Vancouver businesses can fully leverage this benefit. If you invest in a $150,000 TPO roof replacement, you may be able to reduce your taxable income by that full amount immediately. This “tax shield” keeps more cash in your pockets for inventory and payroll. It’s a hardworking financial strategy that mirrors the durability of the roofs we install. Just remember that the roof must be completed and in service by December 31 to qualify for that year’s deduction.

Energy Efficiency Rebates in Portland and Vancouver

Local utility providers in the Northwest are currently offering substantial incentives to help businesses transition to energy-efficient systems. For 2026, the Energy Trust of Oregon and Southwest Washington provides an incentive of $2.00 per square foot for new metal building roof insulation. If you’re operating in Washington, utility companies like Avista offer rebates of $1.00 per square foot for upgrading insulation from R11 to R30 or greater. These rebates directly lower the net cost of your commercial roof replacement financing options. Furthermore, the Washington Clean Buildings Performance Standard has set its first compliance deadline for buildings over 220,000 square feet for June 1, 2026. Upgrading to a “cool roof” system like white TPO or PVC doesn’t just earn you a rebate; it helps you meet these mandatory standards while significantly lowering your long-term HVAC costs. Protecting your investment means looking at the sky for rain and the balance sheet for savings.

Preparing Your Business for a Roofing Finance Application

Securing approval for commercial roof replacement financing options involves more than just a high credit score. Lenders view a commercial roof as a critical asset that protects the business’s ability to generate revenue. To ensure a smooth approval process, you need to present a professional case that combines physical evidence of the roof’s condition with a clear picture of your company’s financial health. Following a structured roadmap helps you avoid delays and positions your business as a low-risk borrower for local Northwest lenders.

Step 1: Documenting the Need with a Professional Inspection

Lenders need to see that the investment is necessary and justified. A simple visual check isn’t enough for a major capital expenditure. We recommend obtaining a comprehensive report that uses core samples to check for moisture in the insulation and infrared scans to identify thermal anomalies. These technical details prove the “cost of inaction” discussed earlier. When you present a detailed roof replacement vancouver wa estimate alongside a condition report, you provide the lender with a clear scope of work. This transparency builds immediate trust and ensures the loan amount accurately reflects the facility’s needs.

Step 2: Financial Documentation Checklist

Lenders will typically require a standard package of documents to evaluate your business’s stability. Being prepared with these items can reduce your approval time from weeks to days. Most commercial roof replacement financing options require the following:

- Tax Returns: Two to three years of federal business tax returns.

- Profit and Loss Statements: Current year-to-date P&L and balance sheets.

- Debt Service Coverage Ratio (DSCR): Most lenders look for a ratio of 1.25 or higher, meaning your business generates enough net operating income to cover its debt obligations comfortably.

- Business Narrative: A brief explanation of how the new roof protects inventory, maintains tenant satisfaction, or meets the Washington Clean Buildings Performance Standard.

Using an estimate from a reputable commercial roofing portland contractor also adds weight to your application. Lenders prefer working with established local companies that have a track record of completing projects on time and within budget. This professional association reduces the lender’s perceived risk regarding the project’s completion. If you are ready to document your building’s needs for a lender, schedule a professional commercial roof inspection to get the data you need for a successful application.

Why Advanced Roofing is Your Strategic Partner in the PNW

Choosing between different commercial roof replacement financing options is a significant decision that impacts your business’s stability for decades. For over 40 years, Advanced Roofing has served the Portland and Vancouver metro areas as a family-owned business. We believe that a roof is more than just a line item on a budget; it is the primary shield for your inventory, your employees, and your livelihood. Our team approaches every project with the integrity of a master craftsman and the approachability of a trusted neighbor. We don’t believe in high-pressure sales tactics. Instead, we focus on providing the technical data and honest assessments you need to make an informed choice for your facility.

Our long history in the Northwest has allowed us to build strong relationships with local lenders and finance specialists who understand the unique needs of property owners in our region. We can help you navigate the documentation requirements for various loan programs, ensuring that your technical roof reports align with what underwriters need to see. This collaborative approach simplifies the path to securing a new, warrantied roof while you focus on running your core business operations.

Local Expertise in the Portland-Vancouver Metro

Operating in the Pacific Northwest requires specialized knowledge of how persistent rain and wind impact different roofing materials. We have extensive experience installing and maintaining diverse commercial systems, including high-reflectivity TPO, durable EPDM, and long-lasting metal roofing. We understand local building codes and the specific drainage requirements necessary to prevent ponding water on flat roof systems. Our reputation for “quality you can trust” stems from our commitment to using premium materials and meticulous flashing details that stand up to our damp climate. We also stay ahead of regional regulations, such as the Washington Clean Buildings Performance Standard, helping you meet the June 1, 2026, compliance deadline for larger facilities through energy-efficient upgrades.

Your Next Steps to a Secure Facility

Protecting your investment starts with a clear understanding of your roof’s current condition and the financial avenues available to you. We offer a straightforward consultation process where we match material specifications to your specific budget and tax strategy. Whether you’re looking to maximize the Section 179 deduction or tap into utility rebates from the Energy Trust of Oregon, we provide the detailed estimates required to move forward. Our goal is to provide peace of mind through transparent communication and a steady, logical path to a dry building. If you’re ready to explore commercial roof replacement financing options for your property, get a detailed commercial roof inspection and estimate today. We’ll show up on time, provide an honest assessment, and stand behind our work for years to come.

Protecting Your Commercial Investment for the Long Term

Choosing the right path for your facility doesn’t have to be a stressful hurdle for your cash flow. By leveraging the latest commercial roof replacement financing options, you can turn a necessary maintenance project into a strategic financial win. You’ve learned how Section 179 tax benefits can offset initial costs and why proactive replacement is the best defense against the persistent Northwest rain. A new roof is more than a structural upgrade; it’s a commitment to the safety of your inventory, the comfort of your tenants, and the stability of your business operations.

Advanced Roofing has been a family-owned and operated cornerstone of the community since 1980. With over 40 years of PNW expertise, we’re fully licensed, bonded, and insured to handle the most complex commercial systems. We’re here to provide the steady guidance you need to navigate both the physical and financial aspects of your project. Don’t let another rainy season threaten your building’s integrity. Request a Free Commercial Roof Estimate & Financing Consultation today. Let’s work together to keep your business dry and your capital protected for years to come.

Frequently Asked Questions

Does a commercial roof replacement qualify for Section 179 in 2026?

Yes, commercial roof replacements qualify for the Section 179 deduction. For the 2026 tax year, businesses can expense up to $2,560,000 for qualifying property improvements. This allows you to deduct the full cost of the project in the first year instead of depreciating it over 39 years. It’s a strategic way to reduce your taxable income while securing your facility against the Northwest rain. The roof must be in service by December 31 to qualify.

What is the typical interest rate for a commercial roofing loan?

Interest rates vary based on the specific commercial roof replacement financing options you select. Conventional commercial loans currently range from 5.40% to 8.84% as of May 2026. SBA 504 loans offer rates between 5.88% and 6.02%, while contractor-arranged financing through local credit unions often starts around 7.99% APR. These fixed rates provide the stability you need to manage facility costs without worrying about market fluctuations or unexpected credit line changes.

Can I finance a commercial roof if my business has a low credit score?

You can still secure funding by choosing specialized programs that look beyond traditional credit scores. C-PACE financing is an excellent choice because it’s based on your property’s value and equity rather than your business credit history. SBA loans also offer more flexible requirements for businesses that don’t meet conventional bank standards. Providing a professional roof condition report can strengthen your application by proving the project is a necessary investment to protect the asset’s value.

How long does the financing approval process usually take?

The timeline for approval depends on the loan type you choose. Equipment Financing Agreements (EFAs) are the fastest, often providing a decision within 24 to 48 hours. Traditional bank loans and SBA-guaranteed programs are more thorough and typically require several weeks for underwriting and documentation. We recommend starting the process early in the spring. This ensures your funding is ready and your project is scheduled before the heavy autumn rains begin in the Vancouver metro area.

Is it better to lease or buy a commercial roofing system?

Most Northwest business owners find that buying is the more strategic financial move. While leasing can offer lower initial payments, buying allows you to take full advantage of the Section 179 tax deduction and build equity in your property. Owning the system outright gives you full control over maintenance and long-term warranties. Buying also avoids the complexities of lease-end negotiations and ensures your facility’s protection is a permanent asset rather than a temporary arrangement.

Are there specific grants or loans for energy-efficient commercial roofs in Oregon?

Oregon and Southwest Washington businesses have access to substantial energy-efficiency incentives. The Energy Trust of Oregon provides a rebate of $2.00 per square foot for qualifying roof insulation upgrades in 2026. Additionally, C-PACE financing is available in many local counties to fund 100% of energy-efficient projects. These incentives help offset the cost of high-performance materials like white TPO, which reduces your building’s cooling load and meets the latest regional energy standards.

Can I include the cost of roof maintenance in my financing package?

Many commercial roof replacement financing options allow you to wrap the entire project scope into a single loan. This can include the core replacement, enhanced insulation, and initial roof certification costs. Including these ancillary services ensures your entire system is protected and warrantied from the start. It simplifies your bookkeeping by keeping all facility-related improvements under one predictable monthly payment that aligns with your business’s revenue cycles and long-term maintenance strategy.

What happens to the financing if I sell the commercial property?

The outcome depends on how your loan is structured. Traditional commercial and SBA loans are typically settled at closing using the proceeds from the sale. However, C-PACE financing is unique because the obligation is tied to the property’s tax assessment. In many cases, the remaining balance can transfer to the new owner. Since the new owner benefits from the energy-efficient roof and its long-term protection, they simply continue the payments through their property tax bill.